Leases in the European life sciences sector run long. Across 154 transactions in our dataset where the original contractual lease term was documented, 81 per cent run to 10 years or longer, and the average lease length is 12.8 years.

Within the long-lease category (10 years or more), our sample gravitates towards a small number of standard durations. Five lease lengths (10, 12, 15, 20 and 25 years) account for 73 per cent of all deals. The single most common term is 10, followed by 15, 20, 12 and 25. This clustering around round-number terms reflects a high degree of standardisation in how life sciences leases are structured.

In the map below, click on a location to see the number of lease transactions.

Why life sciences leases are long

The length of life sciences leases reflects the economics and regulatory structure of the sector more than negotiating convention. Occupiers of R&D, production and clinical facilities invest heavily in specialised infrastructure — cleanrooms, biosafety cabinets, controlled-environment manufacturing suites and advanced HVAC systems — which requires significant capital and takes years to amortise. As a result, they seek long tenure before committing to fit-out. Regulatory requirements reinforce this: operations are tied to licensed premises, making relocation both costly and time-consuming.

On the supply side, developers of purpose-built life sciences space face long planning and construction timelines and require durable rental income to proceed. Long leases are therefore a structural feature of the sector.

The longest leases are single-occupier commitments

Among the 20‑year‑plus leases in our sample, the great majority (around four‑fifths) are single‑tenant commitments: a sole tenant taking a whole building, frequently through a sale-and-leaseback or a built-to-suit development. Multi-let buildings, by contrast, cluster around 10 years and seldom exceed 15.

The mechanism is the same one that makes the sector long-lease in the first place. A 20 or 30 year term is usually bundled with a building that is purpose-configured for, and operationally essential to, one occupier: a bespoke laboratory, a manufacturing plant, a licensed clinical facility. Sale-and-leaseback is a popular route: the operator releases capital while retaining control of a site it cannot easily leave, and the investor underwrites durable, often inflation-linked income.

In a multi-let building, terms are shorter and staggered to preserve flexibility and spread covenant risk across occupiers. But there are nuances. A building leased to two or maybe three occupiers rather than single-let can still support a long average unexpired lease term. For example, in 2025 AEW Europe bought an asset in Munich that had a reported WAULT of c. 10 years, being fully let to three international leading life sciences companies.

Bigger buildings carry longer leases

Splitting the life sciences deals into three size bands shows a clear step-up: the smallest assets (up to around 2,300 sq m) average 10.3 years; mid‑sized (around 2,400–6,400 sq m) 12.2 years; and the largest (above 6,400 sq m) 14.4 years. As in the wider commercial market, longer leases are more common on larger or higher‑value properties. This pattern is particularly evident for single‑tenant sale‑and‑leasebacks and build‑to‑suit assets, which are typically sizeable facilities let on long net‑lease terms to corporate occupiers.

A cross-sector structure, not a life-sciences quirk

This single-occupier, long-income structure is well established beyond life sciences. The same arrangement, one operator on a long, possibly inflation-linked lease of a building integral to its business, can feature 20 to 30-year terms in supermarkets, hotels, car dealerships, care homes and education facilities.

In 2025, UK supermarket Asda executed a £568 million sale‑and‑leaseback of 24 supermarkets and a depot, entering into 25‑year leases (with 10‑year extension options).

Specialist long-income investors are therefore not confined to a single niche segment; they pursue the same single-let, long-income structure wherever it appears, and life sciences is one instance of it rather than a category apart.

Comparison with other sectors (UK)

Against this backdrop, lease lengths in mainstream commercial real estate look markedly different to life sciences. Half of all new commercial leases in the UK have a length of five years or less, according to the Property Data Report 2023 published by the Property Industry Alliance, and the average term is nine years.

Our dataset shows that UK life sciences leases run longer than UK commercial property at large: more than three in four extend to 10 years or more, against fewer than one in five running beyond 10 years across the wider UK market. For UK life sciences specifically, the average term is 11.4 years (12.8 years is the average across the full European sample).

Comparison with other sectors (non-UK)

Across continental Europe, mainstream commercial leases most often fall into short‑ to mid‑range durations. Office and retail leases are commonly structured in 3‑ to 7‑year or 5‑year blocks, with renewal options, although longer fixed terms are agreed for larger or single‑tenant units. In France and Belgium, the dominant form is the statutory 3/6/9 commercial lease — a 9‑year term breakable by the tenant every three years. Office leases in markets such as Luxembourg typically run 3 to 9 years, stretching to 12 to 15 years for major transactions involving significant fit‑out, with six‑ and nine‑year terms particularly prevalent. Logistics leases tend to be shorter for existing stock and longer for new purpose‑built facilities, with 5‑ to 10‑year terms common on modern single‑tenant assets.

Our dataset shows that life sciences leases run longer: more than four in five extend to 10 years or more, and the average term reaches almost 14 years.

Life sciences lease lengths by building type

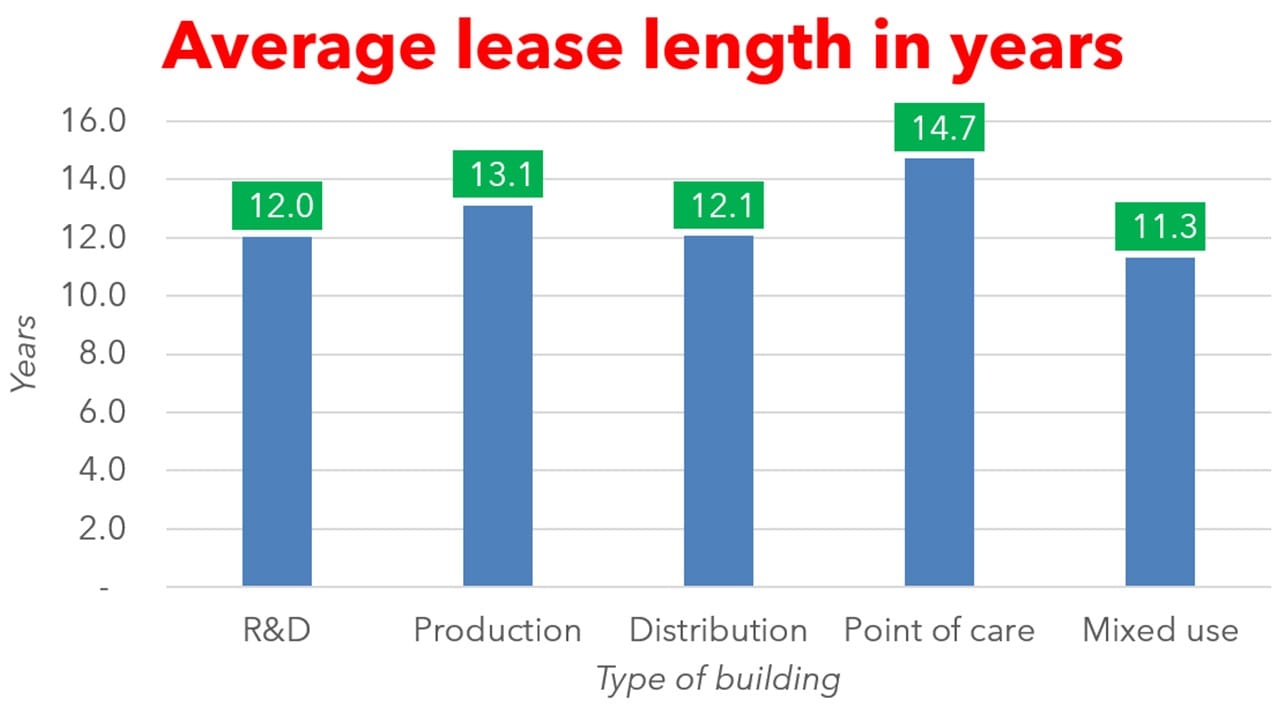

Within the life sciences sector, there are five main types of building: research and development (R&D), production, distribution, point of care and mixed use. Long leases are a consistent feature across all five types, though average lengths vary, as shown in the chart above.

Point of care shows the longest average lease at 14.7 years. This is consistent with the particular sensitivity of clinical environments to disruption: approved premises are tied to regulatory licences, and the cost of relocating a clinical operation is high. The other types sit in the 11.3 to 13.1 years range.

Examples of institutional investment in each type of life sciences building

Point of care

In 2025, Belgian healthcare property specialist Aedifica committed €26.5 million to a forward-funding project for a cancer centre in Limerick. The parties agreed a 30-year CPI-indexed triple-net lease, delivering an initial net rental yield of approximately 7 per cent. The occupier is a specialist oncology operator.

Production

In 2023, Kadans Science Partner acquired Harrow House, a purpose‑built viral‑vector manufacturing facility in Oxford, from Oxford Biomedica in an estimated £4.5 million (€5.1 million) sale‑and‑leaseback deal, with Oxford Biomedica leasing back the building on a 15-year term.

Distribution

In 2024, Clarion Partners acquired a 35,000 sq m logistics facility in the UK that is fully let to the pharmaceutical and medical-device distributor Movianto on a 15-year lease. The reported price was £50.8 million.

R&D

In 2021, Fidelity International bought a research and development property at Leiden Bio Science Park in the Netherlands for €54 million, occupied by tenants with leases ranging from 10 to 15 years, including the Netherlands Center for the Clinical advancement of Stem Cell and Gene Therapies.

Mixed use

In 2023, Swiss Life’s subsidiary BEOS AG acquired a 5,200 sq m new‑build in Berlin for €21 million in a sale‑and‑leaseback transaction. Swedish life sciences solutions provider BICO Group AB sold the property, with its subsidiary SCIENION taking a 15‑year lease on the entire building, including a break option after ten years, for use as SCIENION’s headquarters.

Our data

To keep the analysis precise, we restricted it to the 154 transactions where the original lease term was documented — rather than diluting the figures with partial or unexpired-term records. These deals span the full range of countries and building types.

The lease-length analysis here is one worked example of what the data can show: when we last ran it in October 2024 it drew on 76 leases; this version draws on 154, the sample having doubled as the database has grown.

Summary

Real estate investors seeking long income should look to European life sciences, where, in our pan‑European lease sample, four in five leases run to 10 years or more and the average term approaches 13 years.